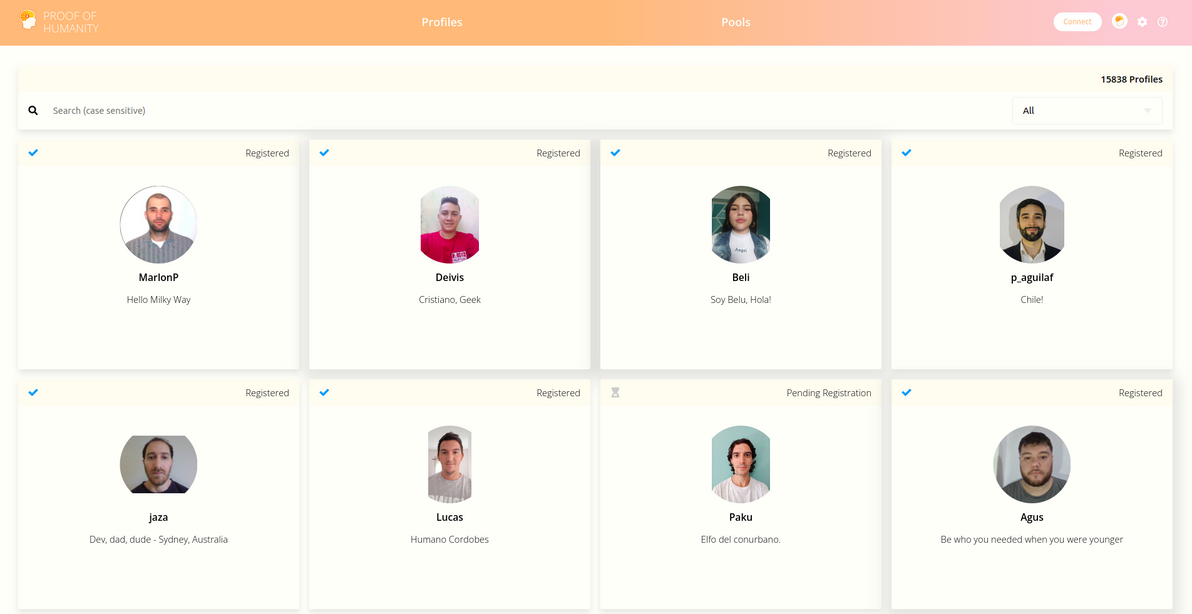

economics - GreenAshPoignant wit and hippie ramblings that are pertinent to economicshttps://greenash.net.au/thoughts/topics/economics/2022-04-19T00:00:00ZOn the Proof of Humanity project2022-04-19T00:00:00Z2022-04-19T00:00:00ZJazahttps://greenash.net.au/thoughts/2022/04/on-the-proof-of-humanity-project/Proof of Humanity (PoH) is a project that I stumbled upon a few weeks ago. Its aim is to create a registry of every living human on the planet. So far, it's up to about 15,000 out of 7 billion.

Just for fun, I registered myself, so I'm now part of that tiny minority who, according to PoH, are verified humans! (Sorry, I guess the rest of you are just an illusion).

Actual bona fide humans

This is a brief musing on the PoH project: its background story, the people behind it, the technology powering it, the socio-economic philosophy behind it, the challenges it's facing, whether it stacks up, and what I think lies ahead.

The story

Most people think of Proof of Humanity in terms of its technology. That is, as a cryptocurrency thing, because it's all built on the Ethereum blockchain. So, yes, it's a crypto project. But, unlike almost every other crypto project, it has little to do with money (although some critics disagree), and everything to do with democracy.

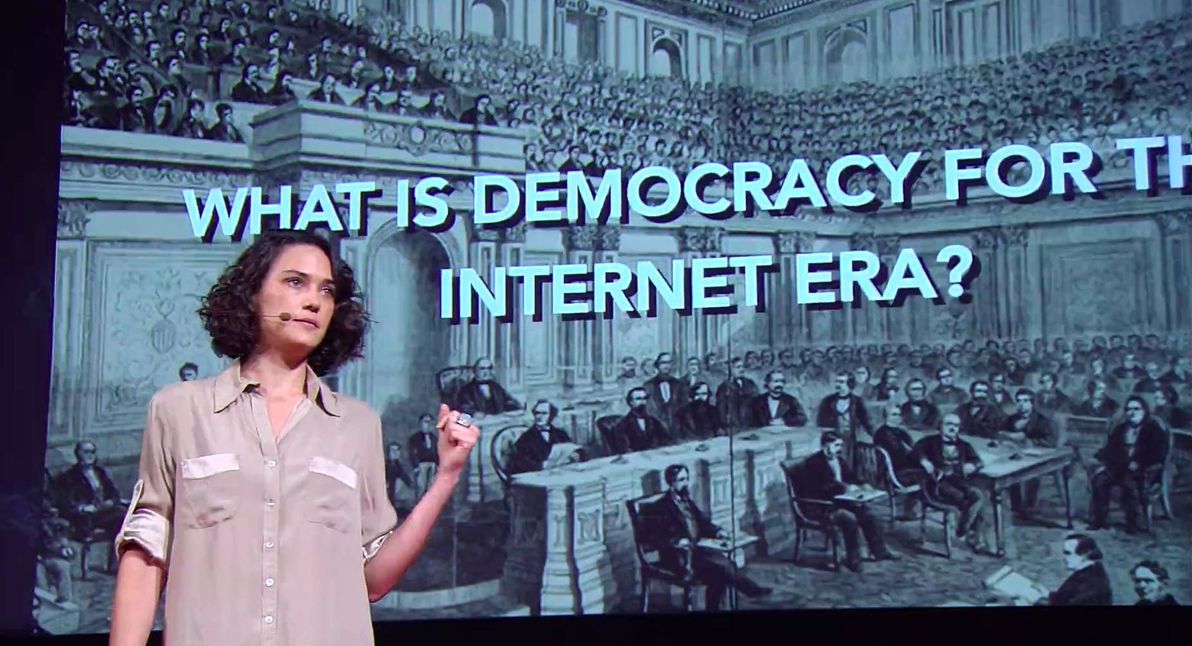

The story begins in 2012, in Buenos Aires, Argentina (a part of the world that I know well and that's close to my heart), when an online voting platform called DemocracyOS was built, and when Pia Mancini founded a new political party called Partido de la Red, which promised it would vote in congress the way constituents told it to vote, law by law (similar to many pirate parties around the world). In 2014, Pia presented all this in a TED talk.

How to upgrade democracy for the Internet era Image source: TED

DemocracyOS – which, by the way, is still alive and kicking – has nothing to do with crypto. It's just a simple voting app. Nor does it handle identity in any innovative way. The pilot in Argentina just relied on voters providing their official government-issued ID documents in order to vote. DemocracyOS is about enabling direct democracy, giving more people a voice, and fighting corruption.

In 2015, Pia Mancini and her partner Santiago Siri – along with Herb Stephens – founded Democracy Earth, which is when crypto entered the mix. The foundation's seminal paper "The Social Smart Contract" laid down (in exhaustive detail) the technical design for a new voting platform based on blockchain. The original plan was for the whole thing to be built on Bitcoin (Ethereum was brand-new at the time).

(Side note: the Democracy Earth paper was actually the thing that I stumbled across, while googling stuff related to direct democracy and liquid democracy. It was only that paper, that then led me to discover Proof of Humanity.)

To make the voting platform feasible, the paper argued, a decentralised "Proof of Identity" solution was needed – the design that the paper spells out for such a system, is clearly the "first draft" of what would later become Proof of Humanity. The paper also presents the spec for a universal basic income being paid to everyone on the platform, which is one of the key features of PoH today.

When Pia and Santiago welcomed their daughter Roma Siri into the world in 2015, they gave her the world's first ever "blockchain valid birth certificate" (using the Bitcoin blockchain). The declaration stated verbally in the video, and the display of the blockchain address in the visual recording, are almost exactly the same as the declaration and the public key that are present in the thousands of PoH registration videos to date.

Roma Siri: the world's first blockchain verified human

The original plan was for Democracy Earth itself to build a blockchain-based voting platform. Which they did: it was called Sovereign, and it launched in 2016. Whereas DemocracyOS enables direct democracy, Sovereign takes things a step further, and enables liquid democracy.

From right: Santiago Siri, Federico Ast, Paula Berman, and Juan Llanos, at the "first Proof of Humanity meetup" in Osaka, Japan, Oct 2019 Image source: Twitter

And fast-forward again to 2021. Proof of Humanity is launched, as an Ethereum Dapp ("decentralised app"). Officially, PoH is independent of any "real-life" people or organisations, and is purely governed by a DAO ("decentralised autonomous organisation").

The main selling point that PoH has pitched so far, is that everyone who successfully registers receives a stream of UBI tokens, which will (apparently!) reduce world poverty and global inequality.

PoH participants are also able to vote on "HIPs" (Humanity Improvement Proposals) – i.e. proposed changes to the PoH smart contract, so basically, equivalent to voting on pull requests for the project's main codebase – I've already cast my first vote. Voting is powered by Snapshot, which appears to be the successor platform to Sovereign – but I'm waiting for someone to reply to my question about that.

PoH is still in its infancy. It doesn't even have a Wikipedia page yet. I wrote a draft Proof of Humanity Wikipedia page, but, despite a lengthy argument with the moderators, I wasn't able to get it published, because apparently there's still insufficient reliable independent coverage of the project. You're welcome to add more sources, to try and satisfy the pedantic gatekeepers over there.

Challenges

By far the biggest challenge to the growth and the success of Proof of Humanity right now, is the exorbitant transaction fees (known as "gas fees") charged by the Ethereum network. Considering that its audience is (ostensibly) every human on the planet, you'd think that registering with PoH would be free, or at least very cheap. Think again!

You have to pay a deposit, which is currently 0.125 ETH (approximately $400 USD), and which is refunded once your profile is successfully verified (and believe me or not, but I'm telling you from personal experience, they do refund it). That amount isn't trivial, even for a privileged first-worlder like myself.

But you also, in my personal experience, have to pay at least another 10% on top of that (i.e. 0.012 ETH, or $40 USD), in non-refundable gas fees, to cover the estimated processing power required to execute the PoH smart contract for your profile. Plus another 10% or so (could well be more, depending on your circumstances) if you need to exchange fiat money for Ethereum, and back again, in order to pay the deposit and to recover it later.

So, a $400 USD deposit, which you lose if your profile is challenged (and your appeal fails), and which takes at least a week to get refunded to you. Plus $80 USD in fees. Plus it's all denominated in a highly volatile cryptocurrency, whose value could plummet at any time. That's a pretty steep price tag, for participation in "a cool experiment" that has no real-world utility right now. Would I spend that money and effort again, to renew my PoH profile when it expires in two years' time? Unless it gains some real-world utility, probably not.

Also a major challenge, is the question of how to give the UBI tokens any real value. UBI can be traded on the open market (although the only exchange that actually allows it to be bought and sold right now is the Argentinian Ripio). When Proof of Humanity launched in early 2021, 1 UBI was valued at approximately $1 USD. Since then, its value has consistently declined, and 1 UBI is now valued at approximately $0.04 USD.

UBI is highly inflationary by design. Every verified PoH profile results in 1 UBI being minted per hour. So every time the number of verified PoH profiles doubles, the rate of UBI minting doubles. And currently there's zero demand for UBI, because there's nothing useful that you can do with it (including investing or speculating in it!). The PoH community is actively discussing possible solutions, but there's no silver bullet.

To top it all off, it's still not clear whether or not PoH will live up to its purported aim, which is to create a Sybil-proof list of humans. The hypothesis underpinning it all, is that a video submission – featuring visual facial movement, and verbal narration – is too high a bar for AI to pass. Deepfake technology, while still in its infancy, is improving rapidly. PoH is betting on Deepfake's capability plateauing below that bar. Time will tell how that gamble unfolds.

PoH is also placing enormous trust in each member of the community of already-verified humans, to vet new profile submissions as representing real, unique humans. It's a radical and unproven experiment. That level of trust has traditionally been reserved for nation-states and their bureaucracies. There are defences built-in to PoH, but time will tell how resilient they are.

Musings

I'm not a crypto guy. The ETH that I bought in order to pay the PoH deposit, is my first ever cryptocurrency holding (and, in keeping with conservative mainstream advice, it's a modest amount, not more than I can afford to lose).

My interest in PoH is from a democratic empowerment point of view, not from a crypto nor a financial point of view. The founders of PoH claim to have the same underlying interest at heart. If that's so, then I'm afraid I don't really understand why they built it all on top of Ethereum, which is, at the end of the day, a financial instrument.

Sure, the PoH design relies on hash proofs, and it requires some kind of blockchain. But they could have built a new blockchain specifically for PoH, one that's not a financial instrument, and one that's completely free as in beer. Instead, they've built a system that's coupled to the monetary value of, at the mercy of the monetary fees of, and vulnerable to the monetary fraud / scams of, the underlying financial network.

Regarding UBI: I think I'm a fan of it – I more-or-less wrote a universal basic income proposal myself, nine years ago. Not unlike what PoH has done, I too proposed that a UBI should be issued in a new currency that's not controlled by any sovereign nation-state (although what I had in mind was that it be governed by some UN-like body, not by something as radical as a DAO).

However, I can't say I particularly like the way that "self-sovereignty" and UBI have been conflated in PoH. I would have thought that the most important use case for PoH would be democratic voting, and I feel that the whole UBI thing is a massive distraction from that. What's more, many of the people who have registered with PoH to date, have done so hoping to make a quick buck with UBI, and is that really the group of people we want, as the pioneers of PoH? (Plus, I hate to break it to you, all you folks banking on UBI, but you're going to be disappointed.)

So, do I think PoH "stacks up"? Well, it's not a scam, although clearly all the project's founders are heavily invested in crypto, and do stand to gain from the success of anything crypto-related. Call me naïve, but I think the people behind PoH are pure of heart, and are genuinely trying to make the world a better place. I can't say I agree with all their theories, but I applaud their efforts.

Just needed to add broccoli Image source: Meme Creator

And do I think PoH will succeed? If it can overcome the critical challenges that it's currently facing, then it stands some chance of one day reaching a critical mass, and of proving itself at scale. Although I think it's much more likely that it will remain a niche enclave. I'd be pleasantly surprised if PoH reaches 5 million users, which would be about 0.1% of internet-connected humanity, still a far cry from World Domination™.

Say what you will about it, Proof of Humanity is a novel, fascinating idea. Regardless of whether it ultimately succeeds in its aims, and regardless of whether it even can or should do so, I think it's an experiment worth conducting.

]]>

How successful was the 20th century communism experiment?2017-11-28T00:00:00Z2017-11-28T00:00:00ZJazahttps://greenash.net.au/thoughts/2017/11/how-successful-was-the-20th-century-communism-experiment/

During the course of the 20th century, virtually every nation in the world was affected, either directly or indirectly, by the "red tide" of communism. Beginning with the Russian revolution in 1917, and ostensibly ending with the close of the Cold War in 1991 (but actually not having any clear end, because several communist regimes remain on the scene to this day), communism was and is the single biggest political and economic phenomenon of modern times.

Communism – or, to be more precise, Marxism – made sweeping promises of a rosy utopian world society: all people are equal; from each according to his ability, to each according to his need; the end of the bourgeoisie, the rise of the proletariat; and the end of poverty. In reality, the nature of the communist societies that emerged during the 20th century was far from this grandiose vision.

Communism obviously was not successful in terms of the most obvious measure: namely, its own longevity. The world's first and its longest-lived communist regime, the Soviet Union, well and truly collapsed. The world's most populous country, the People's Republic of China, is stronger than ever, but effectively remains communist in name only (as does its southern neighbour, Vietnam).

However, this article does not seek to measure communism's success based on the survival rate of particular governments; nor does it seek to analyse (in any great detail) why particular regimes failed (and there's no shortage of other articles that do analyse just that). More important than whether the regimes themselves prospered or met their demise, is their legacy and their long-term impact on the societies that they presided over. So, how successful was the communism experiment, in actually improving the economic, political, and cultural conditions of the populations that experienced it?

Communism: at least the party leaders had fun! Image source:FunnyJunk.

Success:

Health care in Cuba (internationally recognised as being one of the world's best and most accessible public health care systems)

The arts (Soviet theatre and Soviet ballet received funding and support for many years, as Cuban theatre still does; despite severely limiting artistic freedom, most communist regimes did actually make the arts thrive with subsidies)

Education (despite the heavy dose of propaganda in schools, almost all communist regimes have massively improved their populations' literacy rates, and have invested heavily in more schools and universities, and in universal access to them)

Industrialisation (putting aside for a moment the enormous sacrifices made to achieve it, the fact is that the USSR, China, and Vietnam transformed rapidly from agrarian economies into industrial powerhouses under communism, and they remain world industrial heavyweights today)

Freedom (all communist states so far in history have been totalitarian regimes, and have severely curtailed all freedoms – of speech, of movement, of artistic expression, of religion – and that oppressive legacy lives on to this day)

Corruption (far from the Marxist ideal of universal equality, it has most definitely been a case of some are more equal than others in communist states – communism has engendered endemic bribery and nepotism every time)

Human damage (rather than making everyone a winner, communism has generally made almost everyone a victim – as well as the huge number of people murdered, imprisoned, and tortured as enemies of a communist state, almost all citizens other than Party elites have endured prolonged suffering due to the states' constant intrusion into their lives)

Dudes, don't leave a comrade hanging. Image source:FunnyJunk.

Closing remarks

Personally, I have always considered myself quite a "leftie": I'm a supporter of socially progressive causes, and in particular, I've always been involved with environmental movements. However, I've never considered myself a socialist or a communist, and I hope that this brief article on communism reflects what I believe are my fairly balanced and objective views on the topic.

Based on my list of pros and cons above, I would quite strongly tend to conclude that, overall, the communism experiment of the 20th century was not successful at improving the economic, political, and cultural conditions of the populations that experienced it.

I'm reluctant to draw comparisons, because I feel that it's a case of apples and oranges, and also because I feel that a pure analysis should judge communist regimes on their merits and faults, and on theirs alone. However, the fact is that, based on the items in my lists above, much more success has been achieved, and much less failure has occurred, in capitalist democracies, than has been the case in communist states (and the pinnacle has really been achieved in the world's socialist democracies). The Nordic Model – and indeed the model of my own home country, Australia – demonstrates that a high quality of life and a high level of equality are attainable without going down the path of Marxist Communism; indeed, arguably those things are attainable only if Marxist Communism is avoided.

I hope you appreciate what I have endeavoured to do in this article: that is, to avoid the question of whether or not communist theory is fundamentally flawed; to avoid a religious rant about the "evils" of communism or of capitalism; and to avoid judging communism based on its means, and to instead concentrate on what ends it achieved. And I humbly hope that I have stuck to that plan laudably. Because if one thing is needed more than anything else in the arena of analyses of communism, it's clear-sightedness, and a focus on the hard facts, rather than religious zeal and ideological ranting.

]]>

The Jobless Games2017-03-19T00:00:00Z2017-03-19T00:00:00ZJazahttps://greenash.net.au/thoughts/2017/03/the-jobless-games/

There is growing concern worldwide about the rise of automation, and about the looming mass unemployment that will logically result from it. In particular, the phenomenon of driverless cars – which will otherwise be one of the coolest and the most beneficial technologies of our time – is virtually guaranteed to relegate to the dustbin of history the "paid human driver", a vocation currently pursued by over 10 million people in the US alone.

Them robots are gonna take our jobs! Image source:Day of the Robot.

Most discussion of late seems to treat this encroaching joblessness entirely as an economic issue. Families without incomes, spiralling wealth inequality, broken taxation mechanisms. And, consequently, the solutions being proposed are mainly economic ones. For example, a Universal Basic Income to help everyone make ends meet. However, in my opinion, those economic issues are actually relatively easy to address, and as a matter of sheer necessity we will sort them out sooner or later, via a UBI or via whatever else fits the bill.

The more pertinent issue is actually a social and a psychological one. Namely: how will people keep themselves occupied in such a world? How will people nourish their ambitions, feel that they have a purpose in life, and feel that they make a valuable contribution to society? How will we prevent the malaise of despair, depression, and crime from engulfing those who lack gainful enterprise? To borrow the colourful analogy that others have penned: assuming that there's food on the table either way, how do we head towards a Star Trek rather than a Mad Max future?

Keep busy

The truth is, since the Industrial Revolution, an ever-expanding number of people haven't really needed to work anyway. What I mean by that is: if you think about what jobs are actually about providing society with the essentials such as food, water, shelter, and clothing, you'll quickly realise that fewer people than ever are employed in such jobs. My own occupation, web developer, is certainly not essential to the ongoing survival of society as a whole. Plenty of other occupations, particularly in the services industry, are similarly remote from humanity's basic needs.

So why do these jobs exist? First and foremost, demand. We live in a world of free markets and capitalism. So, if enough people decide that they want web apps, and those people have the money to make it happen, then that's all that's required for "web developer" to become and to remain a viable occupation. Second, opportunity. It needs to be possible to do that thing known as "developing web apps" in the first place. In many cases, the opportunity exists because of new technology; in my case, the Internet. And third, ambition. People need to have a passion for what they do. This means that, ideally, people get to choose an occupation of their own free will, rather than being forced into a certain occupation by their family or by the government. If a person has a natural talent for his or her job, and if a person has a desire to do the job well, then that benefits the profession as a whole, and, in turn, all of society.

Those are the practical mechanisms through which people end up spending much of their waking life at work. However, there's another dimension to all this, too. It is very much in the interest of everyone that makes up "the status quo" – i.e. politicians, the police, the military, heads of big business, and to some extent all other "well to-do citizens" – that most of society is caught up in the cycle of work. That's because keeping people busy at work is the most effective way of maintaining basic law and order, and of enforcing control over the masses. We have seen throughout history that large-scale unemployment leads to crime, to delinquency and, ultimately, to anarchy. Traditionally, unemployment directly results in poverty, which in turn directly results in hunger. But even if the unemployed get their daily bread – even if the crisis doesn't reach let them eat cake proportions – they are still at risk of falling to the underbelly of society, if for no other reason, simply due to boredom.

So, assuming that a significantly higher number of working-age men and women will have significantly fewer job prospects in the immediate future, what are we to do with them? How will they keep themselves occupied?

The Games

I propose that, as an alternative to traditional employment, these people engage in large-scale, long-term, government-sponsored, semi-recreational activities. These must be activities that: (a) provide some financial reward to participants; (b) promote physical health and social well-being; and (c) make a tangible positive contribution to society. As a massive tongue-in-cheek, I call this proposal "The Jobless Games".

My prime candidate for such an activity would be a long-distance walk. The journey could take weeks, months, even years. Participants could number in the hundreds, in the thousands, even in the millions. As part of the walk, participants could do something useful, too; for example, transport non-urgent goods or mail, thus delivering things that are actually needed by others, and thus competing with traditional freight services. Walking has obvious physical benefits, and it's one of the most social things you can do while moving and being active. Such a journey could also be done by bicycle, on horseback, or in a variety of other modes.

How about we all just go for a stroll? Image source:The New Paper.

Other recreational programs could cover the more adventurous activities, such as climbing, rafting, and sailing. However, these would be less suitable, because: they're far less inclusive of people of all ages and abilities; they require a specific climate and geography; they're expensive in terms of equipment and expertise; they're harder to tie in with some tangible positive end result; they're impractical in very large groups; and they damage the environment if conducted on too large a scale.

What I'm proposing is not competitive sport. These would not be races. I don't see what having winners and losers in such events would achieve. What I am proposing is that people be paid to participate in these events, out of the pocket of whoever has the money, i.e. governments and big business. The conditions would be simple: keep up with the group, and behave yourself, and you keep getting paid.

I see such activities co-existing alongside whatever traditional employment is still available in future; and despite all the doom and gloom predictions, the truth is that there always has been real work out there, and there always will be. My proposal is that, same as always, traditional employment pays best, and thus traditional employment will continue to be the most attractive option for how to spend one's days. Following that, "The Games" pay enough to get by on, but probably not enough to enjoy all life's luxuries. And, lastly, as is already the case in most first-world countries today, for the unemployed there should exist a social security payment, and it should pay enough to cover life's essentials, but no more than that. We already pay people sit down money; how about a somewhat more generous payment of stand up money?

Along with these recreational activities that I've described, I think it would also be a good idea to pay people for a lot of the work that is currently done by volunteers without financial reward. In a future with less jobs, anyone who decides to peel potatoes in a soup kitchen, or to host bingo games in a nursing home, or to take disabled people out for a picnic, should be able to support him- or herself and to live in a dignified manner. However, as with traditional employment, there are also only so many "volunteer" positions that need filling, and even with that sector significantly expanded, there would still be many people left twiddling their thumbs. Which is why I think we need some other solution, that will easily and effectively get large numbers of people on their feet. And what better way to get them on their feet, than to say: take a walk!

Large-scale, long-distance walks could also solve some other problems that we face at present. For example, getting a whole lot of people out of our biggest and most crowded cities, and "going on tour" to some of our smallest and most neglected towns, would provide a welcome economic boost to rural areas, considering all the support services that such activities would require; while at the same time, it would ease the crowding in the cities, and it might even alleviate the problem of housing affordability, which is acute in Australia and elsewhere. Long-distance walks in many parts of the world – particularly in Europe – could also provide great opportunities for an interchange of language and culture.

In summary

There you have it, my humble suggestion to help fill the void in peoples' lives in the future. There are plenty of other things that we could start paying people to do, that are more intellectual and that make a more tangible contribution to society: e.g. create art, be spiritual, and perform in music and drama shows. However, these things are too controversial for the government to support on such a large scale, and their benefit is a matter of opinion. I really think that, if something like this is to have a chance of succeeding, it needs to be dead simple and completely uncontroversial. And what could be simpler than walking?

Whatever solutions we come up with, I really think that we need to start examining the issue of 21st-century job redundancy from this social angle. The economic angle is a valid one too, but it has already been analysed quite thoroughly, and it will sort itself out with a bit of ingenuity. What we need to start asking now is: for those young, fit, ambitious people of the future that lack job prospects, what activity can they do that is simple, social, healthy, inclusive, low-impact, low-cost, and universal? I'd love to hear any further suggestions you may have.

]]>

Money: the ongoing evolution2013-04-10T00:00:00Z2013-04-10T00:00:00ZJazahttps://greenash.net.au/thoughts/2013/04/money-the-ongoing-evolution/

In this article, I'm going to solve all the monetary problems of the modern world.

Oh, you think that's funny? I'm being serious.

Alright, then. I'm going to try and solve them. Money is a concept, a product and a system that's been undergoing constant refinement since the dawn of civilisation; and, as the world's current financial woes are testament to, it's clear that we still haven't gotten it quite right. That's because getting financial systems right is hard. If it were easy, we'd have done it already.

I'm going to start with some background, discussing the basics such as: what is money, and where does it come from? What is credit? What's the history of money, and of credit? How do central banks operate? How do modern currencies attain value? And then I'm going to move on to the fun stuff: what can we do to improve the system? What's the next step in the ongoing evolution of money and finance?

Disclaimer: I am not an economist or a banker; I have no formal education in economics or finance; and I have no work experience in these fields. I'm just a regular bloke, who's been thinking about these big issues, and reading up on a lot of material, and who would like to share his understandings and his conclusions with the world.

Ancient history

Money has been around for a while. When I talk about money, I'm talking cash. The stuff that leaves a smell on your fingers. The stuff that jingles in your pockets. Cold hard cash.

The earliest known example of money dates back to the 7th century BC, when the Lydians minted coins using a natural gold-based alloy called electrum. They were a crude affair – with each coin being of a slightly different shape – but they evolved to become reasonably consistent in their weight in precious metal; and many of them also bore official seals or insignias.

From Lydia, the phenomenom of minted precious-metal coinage spread: first to her immediate neighbours – the Greek and Persian empires – and then to the rest of the civilised world. By the time the Romans rose to significance, around the 3rd century BC, coinage had become the norm as a medium of exchange; and the Romans established this further with their standard-issue coins, most notably the Denarius, which were easily verifiable and reliable in their precious metal content.

Money, therefore, is nothing new. This should come as no surprise to you.

What may surprise you, however, is that credit existed before the arrival of money. How can that be? I hear you say. Isn't credit – the business of lending, and of recording and repaying a debt – a newer and more advanced concept than money? No! Quite the reverse. In fact, credit is the most fundamental concept of all in the realm of commerce; and historical evidence shows that it was actually established and refined, well before cold hard cash hit the scene. I'll elaborate further when I get on to definitions (next section). For now, just bear with me.

One of the earliest known historical examples of credit – in the form of what essentially amount to "IOU" documents – is from Ancient Babylonia:

… in ancient Babylonia … common commercial documents … are what are called "contract tablets" or "shuhati tablets" … These tablets, the oldest of which were in use from 2000 to 3000 years B. C. are of baked or sun-dried clay … The greater number are simple records of transactions in terms of "she," which is understood by archaeologists to be grain of some sort.

…

From the frequency with which these tablets have been met with, from the durability of the material of which they are made, from the care with which they were preserved in temples which are known to have served as banks, and more especially from the nature of the inscriptions, it may be judged that they correspond to the medieval tally and to the modern bill of exchange; that is to say, that they are simple acknowledgments of indebtedness given to the seller by the buyer in payment of a purchase, and that they were the common instrument of commerce.

But perhaps a still more convincing proof of their nature is to be found in the fact that some of the tablets are entirely enclosed in tight-fitting clay envelopes or "cases," as they are called, which have to be broken off before the tablet itself can be inspected … The particular significance of these "case tablets" lies in the fact that they were obviously not intended as mere records to remain in the possession of the debtor, but that they were signed and sealed documents, and were issued to the creditor, and no doubt passed from hand to hand like tallies and bills of exchange. When the debt was paid, we are told that it was customary to break the tablet.

We know, of course, hardly anything about the commerce of those far-off days, but what we do know is, that great commerce was carried on and that the transfer of credit from hand to hand and from place to place was as well known to the Babylonians as it is to us. We have the accounts of great merchant or banking firms taking part in state finance and state tax collection, just as the great Genoese and Florentine bankers did in the middle ages, and as our banks do to-day.

Source:What is Money? Original source: The Banking Law Journal, May 1913, By A. Mitchell Innes.

As the source above mentions (and as it describes in further detail elsewhere), another historical example of credit – as opposed to money – is from medieval Europe, where the split tally stick was commonplace. In particular, in medieval England, the tally stick became a key financial instrument used for taxation and for managing the Crown accounts:

A tally stick is "a long wooden stick used as a receipt." When money was paid in, a stick was inscribed and marked with combinations of notches representing the sum of money paid, the size of the cut corresponding to the size of the sum. The stick was then split in two, the larger piece (the stock) going to the payer, and the smaller piece being kept by the payee. When the books were audited the official would have been able to produce the stick with exactly matched the tip, and the stick was then surrendered to the Exchequer.

Tallies provide the earliest form of bookkeeping. They were used in England by the Royal Exchequer from about the twelfth century onward. Since the notches for the sums were cut right through both pieces and since no stick splits in an even manner, the method was virtually foolproof against forgery. They were used by the sheriff to collect taxes and to remit them to the king. They were also used by private individuals and institutions, to register debts, record fines, collect rents, enter payments for services rendered, and so forth. By the thirteenth century, the financial market for tallies was sufficiently sophisticated that they could be bought, sold, or discounted.

It should be noted that unlike the contract tablets of Babylonia (and the similar relics of other civilisations of that era), the medieval tally stick existed alongside an established metal-coin-based money system. The ancient tablets recorded payments made, or debts owed, in raw goods (e.g. "on this Tuesday, Bishbosh the Great received eight goats from Hammalduck", or "as of this Thursday, Kimtar owes five kwetzelgrams of silver and nine bushels of wheat to Washtawoo"). These societies may have, in reality, recorded most transactions in terms of precious metals (indeed, it's believed that the silver shekel emerged as the standard unit in ancient Mesopotamia); but these units had non-standard shapes and were unsigned, whereas classical coinage was uniform in shape, and possessed insignias.

In medieval England, the common currency was sterling silver, which consisted primarily of silver penny coins (but there were also silver shilling coins, and gold pound coins). The medieval tally sticks recorded payments made, or debts owed, in monetary value (e.g. "on this Monday, Lord Snottyham received one shilling and eight pence from James Yoohooson", or "as of this Wednesday, Lance Alot owes sixpence to Sir Robin").

Definitions

Enough history for now. Let's stop for a minute, and get some basic definitions clear.

First and foremost, the most basic question of all, but one that surprisingly few people have ever actually stopped to think about: what is money?

Money itself … is useless until the moment we use it to purchase or invest in something. Although money feels as if it has an objective value, its worth is almost completely subjective.

The seller and the depositor alike receive a credit, the one on the official bank and the other direct on the government treasury, The effect is precisely the same in both cases. The coin, the paper certificates, the bank-notes and the credit on the books of the bank, are all indentical in their nature, whatever the difference of form or of intrinsic value. A priceless gem or a worthless bit of paper may equally be a token of debt, so long as the receiver knows what it stands for and the giver acknowledges his obligation to take it back in payment of a debt due.

Money, then, is credit and nothing but credit. A's money is B's debt to him, and when B pays his debt, A's money disappears. This is the whole theory of money.

Source:What is Money? Original source: The Banking Law Journal, May 1913, By A. Mitchell Innes.

For some, money is a substance in which one may bathe. Image source:DuckTales…Woo-ooo!

I think the first definition is the easiest to understand. Money is a medium of exchange: it has no value in and of itself; but it allows us to more easily exchange between ourselves, things that do have value.

I think the last definition, however, is the most honest. Money is credit: or, to be more correct, money is a type of credit; a credit that is expressed in a uniform, easily quantifiable / divisible / exchangeable unit of measure (as opposed to a credit that's expressed in goats, or in bushels of wheat).

(Note: the idea of money as credit, and of credit as debt, comes from the credit theory of money, which was primarily formulated by Innes (quoted above). This is just one theory of money. It's not the definitive theory of money. However, I tend to agree with the theory's tenets, and various parts of the rest of this article are founded on the theory. Also, it should not be confused with The Theory of Money and Credit, a book from the Austrian School of economics, which asserts that the only true money is commodity money, and which is thus pretty well the opposite extreme from the credit theory of money.)

Which brings us to the next defintion: what is credit?

In the article giving the definition of "money as credit", it's also mentioned that "credit" and "debt" are effectively the same thing; just that the two words represent the two sides of a single relationship / transaction. So, then, perhaps it would make more sense to define what is debt:

Middle English dette: from Old French, based on Latin debitum 'something owed', past participle of debere 'owe'.

A debt is something that one owes; it is one's obligation to give something of value, in return for something that one received.

Conversely, a credit is the fact of one being owed something; it is a promise that one has from another person / entity, that one will be given something of value in the future.

So, then, if we put the two definitions together, we can conclude that: money is nothing more than a promise, from the person / entity who issued the money, that they will give something of value in the future, to the current holder of the money.

Perhaps the simplest to understand example of this, in the modern world, is the gift card typically offered by retailers. A gift card has no value itself: it's nothing more than a promise by the retailer, that they will give the holder of the card a shirt, or a DVD, or a kettle. When the card holder comes into the shop six months later, and says: "I'd like to buy that shirt with this gift card", what he/she really means is: "I have here a written promise from you folks, that you will give me a shirt; I am now collecting what was promised". Once the shirt has been received, the gift card is suddenly worthless, as the documented promise has been fulfilled; this is why, when the retailer reclaims the gift card, they usually just dispose of it.

However, there is one important thing to note: the only value of the gift card, is that it's a promise of being exchangeable for something else; and as long as that promise remains true, the gift card has value. In the case of a gift card, the promise ceases to be true the moment that you receive the shirt; the card itself returns to its original issuer (the retailer), and the story ends there.

Money works the same way, only with one important difference: it's a promise from the government, of being exchangeable for something else; and when you exchange that money with a retailer, in return for a shirt, the promise remains true; so the money still has value. As long as the money continues to be exchanged between regular citizens, the money is not returned to its original issuer, and so the story continues.

So, as with a gift card: the moment that money is returned to its original issuer (the government), that money is suddenly worthless, as the documented promise has been fulfilled. What do we usually return money to the government for? Taxes. What did the government originally promise us, by issuing money to us? That it would take care of us (it doesn't buy us flowers or send us Christmas cards very often; it demonstrates its caring for us mainly with other things, such as education and healthcare). What happens when we pay taxes? The government takes care of us for another year (it's supposed to, anyway). Therefore, the promise ceases to be true; and, believe it or not, the moment that the government reclaims the money in taxes, that money ceases to exist.

The main thing that a government promises, when it issues money, is that it will take care of its citizens; but that's not the only promise of money. Prior to quite recent times, money was based on gold: people used to give their gold to the government, and in return they received money; so, money was a promise that the government would give you back your gold, if you ever wanted to swap again.

In the modern economic system, the governments of the world no longer promise to give you gold (although most governments still have quite a lot of gold, in secret buildings with a lot of fancy locks and many armed guards). Instead, by issuing money these days, a government just promises that its money is worth as much as its economy is worth; this is why governments and citizens the world over are awfully concerned about having a "strong economy". However, what exactly defines "the economy" is rather complicated, and it only gets trickier with every passing year.

So, a very useful side effect of money – as opposed to gift cards – is that as long as the promise of money remains true (i.e. as long as the government keeps taking care of its people, and as long as the economy remains strong), regular people can use whatever money they have left-over (i.e. whatever money doesn't return to the government, at which point it ceases to exist), as a useful medium of exchange in regular day-to-day commerce. But remember: when you exchange your money for a kettle at the shop, this is what happens: at the end of the day, you have a kettle (something of value); and the shop has a promise from the government that it is entitled to something (presumably, something of value).

Recent history

Back to our history class. This time, more recent history. The modern monetary system could be said to have begun in 1694, when the Bank of England was founded. The impetus for establishing it should be familiar to all 21st-century readers: the government of England was deeply in debt; and the Bank was founded in order to acquire a loan of £1.2 million for the Crown. Over the subsequent centuries, it evolved to become the world's first central bank. Also, of great note, this marked the first time in history that a bank (rather than the king) was given the authority to mint new money.

The grand tradition of English banking: The Dawes, Tomes, Mousely, Grubbs, Fidelity Fiduciary Bank. Image source:Scene by scene Mary Poppins.

During the 18th and 19th centuries, and also well into the 20th century, the modern monetary system was based on the gold standard. Under this system, countries tied the value of their currency to gold, by guaranteeing to buy and sell gold at a fixed price. As a consequence, the value of a country's currency depended directly on the amount of gold reserves in its possession. Also, consequently, money at that time represented a promise, by the money's issuer, to give an exact quantity of gold to its current holder. This could be seen as a hangover from ancient and medieval times, when money was literally worth the weight of gold (or, more commonly, silver) of which the coins were composed (as discussed above).

During that same time period, the foundation currency – and by far the dominant currency – of the world monetary system was the British Pound. As the world's strongest economy, the world's largest empire (and hence the world's largest trading bloc), and the world's most industrialised nation, all other currencies were valued relative to the Pound. The Pound became the reserve currency of choice for nations worldwide, and most international transactions were denominated with it.

In the aftermath of World War II, the Allies emerged victorious; but the Pound Sterling met its defeat at long last, at the hands of a new world currency: the US Dollar. Because the War had taken place in Europe (and Asia), the financial cost to the European Allied powers was crippling; North America, on the other hand, hadn't witnessed a single enemy soldier set foot on its soil, and so it was that, with the introduction of the Bretton Woods system in 1944, the Greenback rapidly and ruthlessly conquered the world.

The Dollars are Coming! Image source: The Guardian: Reel history.

Under the Bretton Woods system, the gold standard remained in place: the only real difference, was that gold was now spelled with a capital S with a line through it ($), instead of being spelled with a capital L with a line through it (£). The US Dollar replaced the Pound as the dominant world reserve currency and international transaction currency.

The gold standard finally came to an end when, in 1971, President Nixon ended the direct convertibility of US Dollars to gold. Since then, the USD has continued to reign supreme over all other currencies (although it's been increasingly facing competition). However, under the current system, there is no longer a "other currencies -> USD -> gold" pecking order. Theoretically, all currencies are now created equal; and gold is now just one more commodity on the world market, rather than "the shiny stuff that gives money value".

Since the end of Bretton Woods, the world's major currencies exist in a floating exchange rate regime. This means that the only way to measure a given currency's value, is by determining what quantity of another given currency it's worth. Instead of being tied to the value of a real-life object (such as gold), the value of a currency just "floats" up and down, depending on the fluctuations in that country's economy, and depending on the fluctuations in peoples' relative perceptions of its value.

What we have now

The modern monetary system is a complex beast, but at its heart it consists of three players.

The mythical Hydra, a multi-headed monster. Grandaddy of the modern monetary system, perhaps? Image source:HydraVM.

First, there are the governments of the world. In most countries, there's a department that "represents" the government as a whole, within the monetary system: this is usually called the "Treasury"; it may also be called the Ministry of Finance, among other names. Contrary to what you might think, Treasury does not bring new money into existence (even though Treasury usually governs a country's mint, and thus Treasury is the manufacturer of new physical money).

As discussed in definitions (above), in a "pure" system, money comes into existence when the government issues it (as a promise), and money ceases to exist when the government takes it back (in return for fulfilling a promise). However, in the modern system, the job of bringing new money into existence has been delegated; therefore, money does not cease to exist, the moment that it returns to the government (i.e. the "un-creation" of money has also been delegated).

This delegation allows the government itself to function like any other individual or entity within the system. That is, the government has an "account balance", it receives monetary income (via taxation), it spends money (via its budget program), and it can either be "in the green" or "in the red" (with a strong tendency towards the latter). Thus, the government itself doesn't have to worry too much about the really complicated parts of the modern monetary system; and instead, it can just get on with the job of running the country. The government can also borrow money, to supplement what it receives from taxation; and it can lend money, in addition to its regular spending.

Second, there are these things called "central banks" (also known as "reserve banks", among other names). In a nutshell: the central bank is the entity to which all that stuff I just mentioned gets delegated. The central bank brings new money into existence – officially on behalf of the government; but since the government is usually highly restricted from interfering with the central bank's operation, this is a half-truth at best. It creates new money in a variety of ways. One way – which in practice is usually responsible for only a small fraction of overall money creation, but which I believe is worth focusing on nonetheless – is by buying government (i.e. Treasury) bonds.

Just what is a bond? (Seems we're not yet done with definitions, after all.) A bond is a type of debt (or a type of credit, depending on your perspective). A lends money to B, and in return, B gives A bonds. The bonds are a promise that the debt will be repaid, according to various terms (time period, interest payable, etc). So, bonds themselves have no value: they're just a promise that the holder of the bonds will receive something of value, at some point in the future. In the case of government bonds, the bonds are a promise that the government will provide something of value to their current holder.

But, hang on… isn't that also what money is? A promise that the government will provide something of value to the current holder of the money? So, let me get this straight: the Treasury writes a document (bonds) saying "The government (on behalf of the Treasury) promises to give the holder of this document something of value", and gives it to the central bank; and in return, the central bank writes a document (money) also saying "The government (on behalf of the central bank) promises to give the holder of this document something of value", and gives it to the Treasury; and at the end of the day, the government has more money? Or, in other words (no less tangled): the government lends itself money, and money is also itself a government loan? Ummm… WTF?!

Glad I'm not the only one that sees a slight problem here. Image source:Lol Zone.

Third, there are the commercial banks. The main role of these (private) companies is to safeguard the deposits of, and provide loans to, the general public. The main (original) source of commercial banks' money, is from the deposits of their customers. However, thanks to the practice of fractional reserve banking that's prevalent in the modern monetary system, commercial banks are also responsible for about 95% of the money creation that occurs today; almost all of this private-bank-created money is interest (and principal) from loans. So, yes: money is created out of thin air; and, yes, the majority of money is not created by the government (either on behalf of Treasury or the central bank), but by commercial banks. No surprise, then, that about 97% of the world's money exists only electronically in commercial bank accounts (with physical cash making up the other 3%).

This presents another interesting conundrum: all money supposedly comes from the government, and is supposedly a promise from the government that they will provide something of value; but in today's reality, most of our money wasn't created by the government, it was created by commercial banks! So, then: if I have $100 in my bank account, does that money represent a promise from the government, or a promise from the commercial banks? And if it's a promise from the commercial banks… what are they promising? Beats me. As far as I know, commercial banks don't promise to take care of society; they don't promise to exchange money for gold; I suppose the only possibility is that, much as the government promises that money is worth as much as the nation's economy is worth, commercial banks promise that money is worth as much as they are worth.

And what are commercial banks worth? A lot of money (and not much else), I suppose… which starts taking us round in circles.

I should also mention here, that the central banks' favourite and most oft-used tool in controlling the creation of money, is not the buying or selling of bonds; it's something else that we hear about all the time in the news: the raising or lowering of official interest rates. Now that I've discussed how 95% of money creation occurs via the creation of loans and interest within commercial banks, it should be clear why interest rates are given such importance by government and by the media. The central bank only sets the "official" interest rate, which is merely a guide for commercial banks to follow; but in practice, commercial banks adjust their actual interest rates to closely match the official one. So, in case you had any lingering doubts: the central banks and the commercial banks are, of course, all "in on it" together.

Oh yeah, I almost forgot… and then there are regular people. Just trying to eke out a living, doing whatever's necessary to bring home the dough, and in general trying to enjoy life, despite the best efforts of the multi-headed beast mentioned above. But they're not so important; in fact, they hardly count at all.

In summary: today's system is very big and complex, but for the most part it works. Somehow. Sort of.

Broken promises

In case you haven't worked it out yet: money is debt; debt is credit; and credit is promises.

Bankers, like politicians, are big on promises. In fact, bankers are full of promises (by definition, since they're full of money). And, also like politicians, bankers are good at breaking promises.

Or, to phrase it more accurately: bankers are good at convincing you to make promises (i.e. to take out a loan); and they're good at promising you that you'll have no problem in not breaking your promises (i.e. in paying back the loan); and they're good at promising you that making and not breaking your promises will be really worthwhile for you (i.e. you'll get a return on your loan); and (their favourite part) they're exceedingly good at holding you to your promises, and at taking you to the dry cleaners in the event that you are truly unable to fulfil your promises.

Since money is debt, and since money makes the world go round, the fact that the world is full of debt really shouldn't make anyone raise an eyebrow. What this really means, is that the world is full of promises. This isn't necessarily a bad thing, assuming that the promises being made are fair. In general, however, they are grossly unfair.

Let's take a typical business loan as an example. Let's say that Norbert wants to open a biscuit shop. He doesn't have enough money to get started, so he asks the bank for a loan. The bank lends Norbert a sum of money, with a total repayment over 10 years of double the value of the sum being lent (as is the norm). Norbert uses the money to buy a cash register, biscuit tins, and biscuits, and to rent a suitable shop venue.

There are two possibilities for Norbert. First, he generates sufficient business selling biscuits to pay off the loan (which includes rewarding the bank with interest payments that are worth as much as it cost him to start the business), and he goes on selling biscuits happily ever after. Second, he fails to bring in enough revenue from the biscuit enterprise to pay off the loan, in which case the bank seizes all of his business-related assets, and he's left with nothing. If he's lucky, Norbert can go back to his old job as a biscuit-shop sales assistant.

What did Norbert input, in order to get the business started? All his time and energy, for a sustained period. What was the real cost of this input? Very high: Norbert's time and energy is a tangible asset, which he could have invested elsewhere had he chosen (e.g. in building a giant Lego elephant). And what is the risk to Norbert? Very high: if business goes bad (and the biscuit market can get volatile at times), he loses everything.

What did the bank input, in order to get the business started? Money. What was the real cost of this input? Nothing: the bank pulled the money out of thin air in order to lend it to Norbert; apart from some administrative procedures, the bank effectively spent nothing. And what is the risk to the bank? None: if business goes well, they get back double the money that they lent Norbert (which was fabricated the moment that the loan was approved anyway); if business goes bad, they seize all Norbert's business-related assets (biscuit tins and biscuits are tangible assets), and as for the money… well, they just fabricated it in the first place anyway, didn't they?

Broke(n) nations

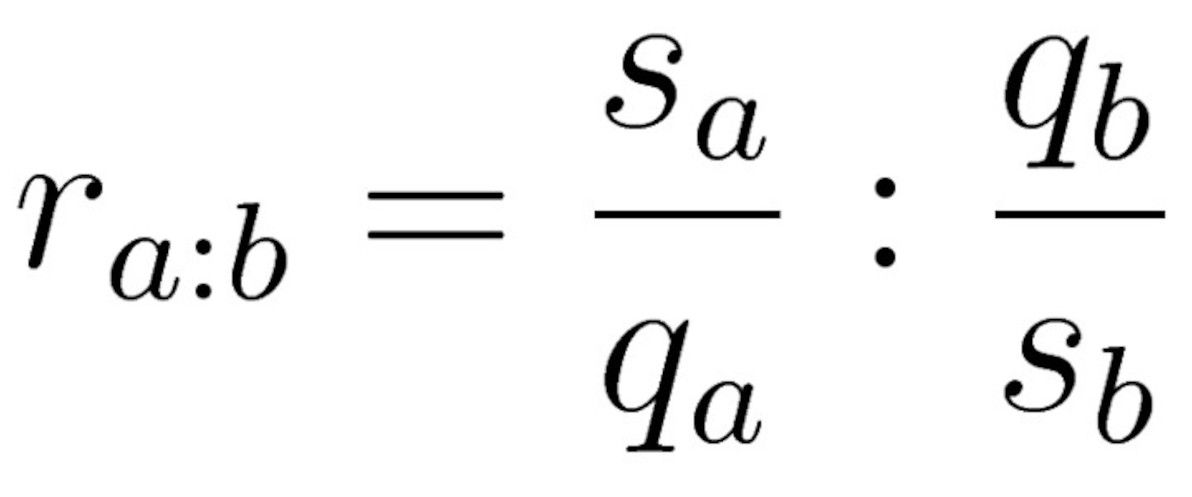

One theme that I haven't touched on specifically so far, is the foreign currency exchange system. However, I've already explained that money is worth as much as a nation's economy is worth; so, logically, the stronger a nation's economy is, the more that nation's money is worth. This is the essence of foreign currency exchange mechanics. Here's a formula that I just invented, but that I believe is reasonably accurate, for determining the exchange rate r between two given currencies a and b:

Where sx is the strength of the given economy, and qx is the quantity of the given currency in existence.

So, for example, say we want to determine the exchange rate of US Dollars to Molvanîan Strubls. Let's assume that the US economy is worth "1,000,000" (which is good), and that there are 1,000,000 US Dollars (a) in existence; and let's assume that the Molvanîan economy is worth "100" (which is not so good), and that there are 1,000,000,000 Molvanîan Strubls (b) in existence. Substituting values into the formula, we get:

This, in my opinion, should be sufficient demonstration of why the currencies of strong economies have value, and why people the world over like getting their hands dirty with them; and why the currencies of weak economies lack value, and why their only practical use is for cleaning certain dirty orifices of one's body.

Or, for a real-world example of a currency worth less than its weight in toilet paper, see Zimbabwe. Image source:praag.org.

Now, getting back to the topic of lending money. Above, I discussed how banks lend money to individuals. As it turns out, banks also lend money to foreign countries. Either commercial banks, central banks, or an international bank (such as the IMF), doesn't matter in this context. And, either foreign individuals, foreign companies, or foreign governments, doesn't matter either in this context. The point is: there are folks whose local currency isn't accepted worldwide (if it's even accepted locally), and who need to purchase goods and services from the world market; and so, these folks ask for a loan from banks elsewhere, who are able to lend them money in a strong currency.

The example scenario that I described above (Norbert), applies equally here. Only this time, Norbert is a group of people from a developing country (let's call them The Morbert Group), and the bank is a corporation from a developed country. As in Norbert's case, The Morbert Group input a lot of time and effort to start a new business; and the bank input money that it pulled out of thin air. And, as in Norbert's case, The Morbert Group has a high risk of losing everything, and at the very least is required to pay an exorbitant amount of interest on its loan; whereas the bank has virtually no risk of losing anything, as it's a case of "the house always wins".

So, the injustice of grossly unfair and oft-broken promises between banks and society doesn't just occur within a single national economy, it occurs on a worldwide scale within today's globalised economy. Yes, the bank is the house; and yes (aside from a few hiccups), the house just keeps winning and winning. This is how, in the modern monetary system, a nation's rich people keep getting richer while its poor people keep getting poorer; and it's how the world's rich countries keep getting richer, while the poor countries keep getting poorer.

Serious problems

Don't ask "how did it come to this?" I've just spent a large number of words explaining how it's come to this (see everything above). Face the facts: it has come to this. The modern monetary system has some very serious problems. Here's my summary of what I think those problems are:

Currency inequality promotes poverty. In my opinion, this is the worst and the most disgraceful of all our problems. A currency is only worth as much as its nation's economy is worth. This is wrong. It means that the people who are issued that currency, participate in the global economy with a giant handicap. It's not their fault that they were born in a country with a weaker economy. Instead, a currency should be worth as much as its nation's people are worth. And all people in all countries are "worth" the same amount (or, at least, they should be).

Governments manipulate currency for their own purposes. All (widely-accepted) currency in the world today is issued by governments, and is controlled by the world's central banks. While many argue that the tools used to manipulate the value of currency – such as adjusting interest rates, and trading in bonds – are "essential" for "stabilising" the economy, it's clear that very often, governments and/or banks abuse these tools in the pursuit of more questionable goals. Governments and central banks (particularly those in "strong" countries, such as the US) shouldn't have the level of control that they do over the global financial system.

Almost all new money is created by commercial banks. The creation of new money should not be entrusted to a handful of privileged companies around the world. These companies continue to simply amass ever-greater quantities of money, further promoting poverty and injustice. Money creation should be more fairly distributed between all individuals and between all nations.

It's no longer clear what gives money its value. In the olden days, money was "backed" by gold. Under the current system, money is supposedly backed by the value of the issuing country's economy. However, the majority of new money today is created by commercial banks, so it's unclear if that's really true or not. Perhaps a new way definition of what "backs" money is needed?

Now, at long last – after much discussion of promises made and promises broken – it's time to fulfil the promise that I made at the start of this article. Time to solve all the monetary problems of the modern world!

Possible solutions

One alternative to the modern monetary system, and its fiat money roots (i.e. money "backed by nothing"), is a return to the gold standard. This is actually one of the more popular alternatives, with many arguing that it worked for thousands of years, and that it's only for the past 40-odd years (i.e. since the Nixon Shock in 1971) that we've been experimenting with the current (broken) system.

This is a very conservative argument. The advocates of "bringing back the gold standard" are heavily criticised by the wider community of economists, for failing to address the issues that caused the gold standard to be dropped in the first place. In particular, the critics point out that the modern world economy has been growing much faster than the world's supply of gold has been growing, and that there literally isn't enough physical gold available, for it to serve as the foundation of the modern monetary system.

Personally, I take the critics' side: the gold standard worked up until modern times; but gold is a finite resource, and it has certain physical characteristics that limit its practical use (e.g. it's quite heavy, it's not easily divisible into sufficiently small parts, etc). Gold will always be a valuable commodity – and, as the current economic crisis shows, people will always turn to gold when they lose confidence in even the most stable of regular currencies – but its days as the foundation of currency were terminated for a reason, and so I don't think it's altogether bad that we relegate the gold standard to the annals of history.

How about getting rid of money altogether? For virtually as long as money has existed, it's been often labelled "the root of all evil". The most obvious solution to the world's money problems, therefore, is one that's commonly proposed: "let's just eliminate money." This has been the cry of hippies, of communists, of utopianists, of futurists, and of many others.

Imagine no possessions... I wonder if you can. Image source:Etsy.

Unfortunately, the most prominent example so far in world history of (effectively) eliminating money – 20th century communism – was also an economic disaster. In the Soviet Union, although there was money, the price of all basic goods and services was fixed, and everything was centrally distributed; so money was, in effect, little more than a rationing token. Hence the famous Russian joke: "We pretend to work, They pretend to pay us".

Utopian science fiction is also rife with examples of a future without money. The best-known and best-developed example is Star Trek (an example with which I'm also personally well-acquainted). In the Star Trek universe, where virtually all of humanity's basic needs (i.e. food, clothing, shelter, education, medicine) are provided for in limitless supply by modern technology, "the economics of the future are somewhat different". As Captain Picard says in First Contact: "The acquisition of wealth is no longer the driving force in our lives. We work to better ourselves and the rest of humanity." This is a great idea in principle; but Star Trek also fails to address the practical issues of such a system, any better than contemporary communist theory does.

Star Trek IV: "They're still using money. We need to get some." Image source:Moar Powah.

While I'm strongly of the opinion that our current monetary system needs reform, I don't think that abolishing the use of money is: (a) practical (assuming that we want trade and market systems to continue existing in some form); or (b) going to actually address the issues of inequality, corruption, and systemic instability that we'd all like to see improved. Abolishing money altogether is not practical, because we do require some medium of exchange in order for the civilised world (which has always been built on trade) to function; and it's not going to address the core issues, because money is not the root of all evil, money is just a tool which can be used for either good or bad purposes (the same as a hammer can be used to build a house or to knock someone on the head – the hammer itself is "neutral"). The problem is not money; the problem is greed.

For a very different sci-fi take on the future of money, check out the movie In Time (2011). In this dystopian work, there is a new worldwide currency: time. Every human being is born with a "biological watch", that shows on his/her forearm how much time he/she has left to live. People can earn time, trade with time, steal time, donate time, and store time (in time banks). If you "time out" (i.e. run out of time), you die instantly.

In Time: you're only worth as many seconds as you have left to live. Image source:MyMovie Critic.

The monetary system presented by In Time is interesting, because it's actually very stable (i.e. the value of "time" is very clear, and time as a currency is quite resilient to inflation / deflation, speculation, etc), and it's a currency that's "backed" by a real commodity (i.e. time left alive; commodities don't get much more vital). However, the system also has gross potential for inequality and corruption – and indeed, in the movie, it's clearly demonstrated that everyone could live indefinitely if the banks just kept rewarding infinte quantities of time; but instead. time is meagerly rationed out by the rich and powerful elite (who can create more time out of thin air whenever they want, much as today's elite do with money), in order to enforce a status quo upon the impoverished masses.

One of the most concerted efforts that has been made in recent times, to disrupt (and potentially revolutionise) the contemporary monetary system, is the much-publicised Bitcoin project. Bitcoin is a virtual currency, which isn't issued or backed by any national government (or by any official organisation at all, for that matter), but which is engineered to mimic many of the key characteristics of gold. In particular, there's a finite supply of Bitcoins; and new Bitcoins can only be created by "mining" them.

Bitcoin makes no secret of the fact that it aims to become a new global world currency, and to bring about the demise of traditional government-issued currency. As I've already stated here, I'm in favour of replacing the current world currencies; and I applaud Bitcoin's pioneering endeavours to do this. Bitcoin sports the key property that I think any contender to the "brave new world of money" would need: it's not generated by central banks, nor by any other traditional contemporary authority. However, there are a number of serious flaws in the Bitcoin model, which (in my opinion) mean that Bitcoin cannot and (more importantly) should not ever achieve this.

Most importantly, Bitcoin fails to adequately address the issue of "money creation should be fairly distributed between all". In the Bitcoin model, money creation is in the hands of those who succeed in "mining" new Bitcoins; and "mining" Bitcoins consists of solving computationally expensive cryptographic calculations, using the most powerful computer hardware possible. So, much as Bitcoin shares many of gold's advantages, it also shares many of its flaws. Much as gold mining unfairly favours those who discover the gold-hills first, and thereafter favours those with the biggest drills and the most grunt; so too does Bitcoin unfairly favour those who knew about Bitcoin from the start, and thereafter favour those with the beefiest and best-engineered hardware.

Mining: a dirty business that rewards the boys with the biggest toys. Image source:adelaidenow.

Bitcoin also fails to address the issue of "what gives money its value". In fact, "what gives Bitcoin its value" is even less clear than "what gives contemporary fiat money its value". What "backs" Bitcoin? Not gold. Not any banks. Not any governments or economies. Supposedly, Bitcoin "is" the virtual equivalent of gold; but then again (as others have stated), I'll believe that the day I'm shown how to convert digital Bitcoins into physical metal chunks that are measured in Troy ounces. It's also not clear if Bitcoin is a commodity or a currency (or both, or neither); and if it's a commodity, it's not completely clear how it would succeed as the foundation of the world monetary system, where gold failed.

Plus, assuming that Bitcoin is the virtual equivalent of gold, the fact that it's virtual (i.e. technology-dependent for its very existence) is itself a massive disadvantage, compared to a physical commodity. What happens if the Internet goes down? What happens if there's a power failure? What happens if the world runs out of computer hardware? Bye-bye Bitcoin. What happens to gold (or physical fiat money) in any of these cases? Nothing.

Additionally, there's also significant doubt and uncertainty over the credibility of Bitcoin, meaning that it fails to address the issue of "manipulation of currency [by its issuers] for their own purposes". In particular, many have accused Bitcoin of being a giant scam in the form of a Ponzi scheme, which will ultimately crash and burn, but not before the system's founders and earliest adopters "jump ship" and take a fortune with them. The fact that Bitcoin's inventor goes by the fake name "Satoshi Nakamoto", and has disappeared from the Bitcoin community (and kept his true identity a complete mystery) ever since, hardly enhances Bitcoin's reputation.

This article is not about Bitcoin; I'm just presenting Bitcoin here, as one of the recently-proposed solutions to the problems of the world monetary system. I've heavily criticised Bitcoin here, to the point that I've claimed it's not suitable as the foundation of a new world monetary system. However, let me emphasise that I also really admire the positive characteristics of Bitcoin, which are numerous; and I hope that one day, a newer incarnation is born that borrows these positive characteristics of Bitcoin, while also addressing Bitcoin's flaws (and we owe our thanks to Bitcoin's creator(s), for leaving us an open-source system that's unencumbered by copyright, patents, etc). Indeed, I'd say that just as non-virtual money has undergone numerous evolutions throughout history (not necessarily with each new evolution being "better" than its predecessors); so too will virtual currency undergo numerous evolutions (hopefully with each new evolution being "better"). Bitcoin is only the beginning.

My humble proposal

The solution that I'd like to propose, is a hybrid of various properties of what's been explored already. However, the fundamental tenet of my solution, is something that I haven't discussed at all so far, and it is as follows:

Every human being in the world automatically receives an "allowance", all the time, all their life. This "allowance" could be thought of as a "global minimum wage"; although everyone receives it regardless of, and separate to, their income from work and investments. The allowance could be received once a second, or once a day, or once a month – doesn't really matter; I guess that's more a practical question of the trade-off in: "the more frequent the allowance, the more overhead involved; the less frequent the allowance, the less accurate the system is."

Ideally, the introduction of this allowance would be accompanied by the introduction of a new currency; and this allowance would be the only permitted manner in which new units of the currency are brought into existence. That is, new units of the currency cannot be generated ad lib by central banks or by any other organisation (and it would be literally impossible to circumvent this, a la Bitcoin, thus making the currency a commodity rather than a fiat entity). However, a new currency is not the essential idea – the global allowance per person is the core – and it could be done with one or more existing currencies, although this would obviously have disadvantages.

The new currency for distributing the allowance would also ideally exist primarily in digital form. It would be great if, unlike Bitcoin and its contemporaries, the currency could also exist in a physical commodity form, with an easy way of transforming the currency between digital and physical form, and vice versa. This would require technology that doesn't currently exist – or, at the least, some very clever engineering with the use of current technology – and is more "wishful thinking" at this stage. Additionally, the currency could also exist as an "account balance" genetically / biologically stored within each person, much like in the movie In Time; except that you don't die if you run out of money (you just ain't got no money). However, all of this is non-essential bells and whistles, supplementing my core proposal.

There are a number of other implementation details, that I don't think particularly need to all be addressed at the conceptual level, but that would be significant at the practical level. For example: should the currency be completely "tamper-proof", or should there be some new international body that could modify various parameters (e.g. change the amount of the allowance)? And should the allowance be exactly the same for everyone, or should it vary according to age, physical location, etc? Personally, I'd opt for a completely "tamper-proof" currency, and for a completely standard allowance; but other opinions may differ.

Taxation would operate in much the same way as it does now (i.e. a government's primary source of revenue, would be taxing the income of its citizens); however, the wealth difference between countries would reduce significantly, because at a minimum, every country would receive revenue purely based on its population.

A global allowance (issued in the form of a global currency), doesn't necessarily mean a global government (although the two would certainly function much better together). It also doesn't necessarily mean the end of national currencies; although national currencies would probably, in the long run, struggle to compete for value / relevance with a successful global currency, and would die out.

If there's a global currency, and a global allowance for everyone on the planet, but still individual national governments (some of which would be much poorer and less developed than others), then taxation would still be at the discretion of each nation. Quite possibly, all nations would end up taxing 100% of the allowance that their citizens receive (and corrupt third-world nations would definitely do this); in which case it would not actually be an allowance for individuals, but just a way of enforcing more economic equality between countries based on population.